An interview with Professor Sharon Collard about the role of credit unions in identifying and supporting members at risk of gambling-related vulnerability.

Money and Gambling: Practice, Insight, Evidence (MAGPIE)

A partnership between the University of Bristol's Personal Finance Research Centre and GambleAware

An interview with Professor Sharon Collard about the role of credit unions in identifying and supporting members at risk of gambling-related vulnerability.

On July 14, GambleAware hosted a webinar on the topic of finance and gambling. During the session, which was chaired by Money and Mental Health CEO, Helen Undy, speakers explored what data and information is available to banks to help protect against and detect possible gambling harms.

Simon McNair from the Behavioural Insights Team also shared highlights from two reports produced using HSBC and Monzo data that examined what customer transactional data can show us about gambling habits.

Professor Sharon Collard from PFRC talked through the new guide for financial institutions, including the main recommendations banks should take forward.

Natalie Ledward from Monzo, also shared her view on the new research and guide, including how it will impact their work going forward to help prevent their customers from experiencing gambling harm.

You can watch the webinar below.

This week the Personal Finance Research Centre and GambleAware published a practical guide for financial services firms seeking to protect customers from gambling-related financial harms.

The guide explores how the UK Financial Conduct Authority’s expectations regarding the fair treatment of vulnerable customers can be applied to harmful gambling. It offers practical examples of how regulated firms are already identifying and supporting customers who are at risk of gambling harm and what more can be done.

You can read the guide or our executive summary here, and watch our short summary video below.

By Sharon Collard

The boom in online investing brings opportunities but also risks – including links between risky investing and gambling problems. The blurring of investing and gambling poses challenges for regulators and businesses that are responsible for protecting consumers from harm.

From a UK perspective, the rise in online investing – boosted by the pandemic – marks an important shift in a population that has stuck doggedly to cash savings even in the face of historically low interest rates. And it is encouraging to see younger adults getting involved in tech-enabled investing, attracted by easy-to-use interfaces and fee-free business models.

At the same time, new trends like meme investing exploit age-old human biases that can exacerbate risk, particularly in the volatile and uncertain times in which we live. People see high-risk activities like cryptocurrency trading (unregulated in the UK) as an exciting fast-track to easy wealth. Investors may conduct little or no research before they buy, instead making snap decisions based on what they hear from social media influencers and short-form trading tips on TikTok. They tend to over-state their own knowledge while also distrusting official sources of information and dismissing regulator’s risk warnings as old-fashioned and downright boring. And it goes without saying that their ‘capital is at risk’ with a good chance of losing most or all the money they invest and a low chance of making money even over the longer-term.

In addition, the academic literature highlights strong links between risky investing and gambling problems. Risky trading can be part of a broader repertoire of gambling activities and studies show links between higher rates of “problem gambling” and high-frequency trading in riskier products like derivatives. There is evidence of “addictive-like trading behaviour” – small early wins followed by loss chasing, where someone can end up losing control over the money they have invested. These risks have been exacerbated during the pandemic with people spending much more time at home where they may be isolated and bored. The national charity GamCare has reported a rise in the number of people asking for help with problems related to day trading on its online forums. The past few days have also seen the fallout from the collapse of Football Index, a gambling platform with an estimated 0.5 million users that marketed itself as a “stockmarket for footballers” – perhaps the most blatant example to date of the blurred line between gambling and investing.

This blurring raises many questions for regulators and businesses about how to protect individuals who may be at risk of significant harm through gambling and high-risk investing. There is also the difficult question of how to regulate an online space awash with unregulated financial advice and increasingly sophisticated investment frauds and scams. For gambling treatment and support professionals, it raises the question of whether high-risk investing should routinely be screened for, and treated as, a subset of gambling disorder. Altogether, this points to the need for better cross-sectoral regulation and collaboration in a world where boundaries are more blurred than ever.

By Katie Cross

It’s Talk Money Week, a fantastic initiative to encourage people to open up about their financial worries. There are many reasons why people don’t like to talk about money but one reason revolves around shame and the concern people have about being judged. This is very relevant when it comes to gambling disorder, sometimes called the ‘hidden’ or ‘invisible’ addiction.

People with gambling disorder don’t present with physical symptoms in the same way as drug or alcohol addiction which can make them difficult to detect. The perceived stigma associated with gambling disorder can lead people to feel ashamed, which may result in them hiding their gambling in order to avoid being judged, and refrain from seeking help or treatment.

It is reported that only 2 in 10 people experiencing harms arising from gambling (17%) sought treatment over the last year, rising to 54% for ‘problem gamblers’. This means that 83% of those experiencing some level of harm from gambling, and around half of ‘problem gamblers’, aren’t seeking support, of which 11% and 27% respectively reported ‘stigma and shame’ as a reason for not doing so. Moreover, this stigma and shame can actually lead to an increase in gambling activity, as gamblers might try to win back the money before a loved one finds out, or gamble more as a way of escaping painful emotions. Therefore, addressing stigma is vital if we want to reduce harm and encourage more people to seek help.

Talking to a loved one about gambling disorder can provide the encouragement needed, with 1 in 5 ‘problem gamblers’ saying this would motivate them to seek support. Although potentially a difficult conversation to initiate, it could make a big difference. The Money and Pensions Service guides offer advice on how to start a conversation about money with a loved one. Not everyone has someone to talk to though, and there are also some great podcasts out there from people with lived experience of gambling harms that aim to offer support to those affected and further our understanding of this complex issue.

In addition, we believe there is a strong rationale for the financial services industry to play a greater role in reducing gambling harms. One obvious way to do this is responsible lending. In addition, having access to transaction data puts financial services firms in a unique position to spot early warning signs of gambling disorder. They have the opportunity to reach out to customers, for example by offering budgeting tools, ATM withdrawal limits, spending limits or bank card gambling blocks, all of which might go some way to reducing gambling harms.

Information and help for people with gambling disorder:

Information and help for people affected by someone else’s gambling:

By Sharon Collard

Talk Money Week aims to increase people’s sense of financial wellbeing by encouraging them to open up about their personal finances. For people with gambling disorder, feelings of stigma and shame can make this challenging. Added to this, harms that arise from gambling are often hidden and only become visible following major crises such as extreme debt or relationship breakdown. These events also have a devastating impact on family members. This blog looks at how financial firms can help people affected by someone else’s gambling.

For every person with a gambling disorder, between six and ten other people are affected. An estimated 7% of Britain’s adult population (around 3.6m people) have personally experienced negative effects from someone else’s gambling – usually someone in their immediate family – with harms arising from gambling impacting their relationships, mental wellbeing and finances.

The gambling literature highlights ways in which affected others can help and support those with gambling disorder. In Singapore, family members can act on behalf of someone with a gambling disorder and arrange for them to be excluded from gambling venues. In New Zealand, gambling outlets receive guidance encouraging them to do all they can to take notifications from third parties (such as family members or friends) into account, as these are one of the most common indicators of gambling harms.

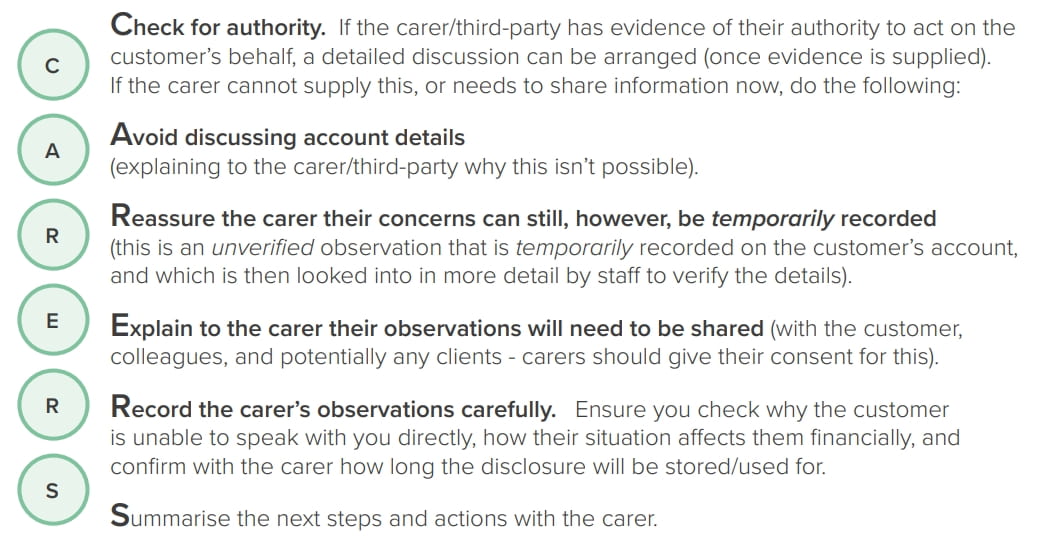

For UK financial services firms – the focus of our MAGPIE programme – this raises questions about whether they might accept requests from affected others to help reduce the financial harm caused by someone else’s gambling, such as activating a bank card gambling block, setting ATM limits or restricting access to credit. New guidance from the Money Advice Liaison Group and the Money Advice Trust sets out the practical actions that firms can take to manage disclosures of vulnerability such as gambling disorder, including disclosures from carers and other third parties, while also taking GDPR into account (Figure 1).

Figure 1: The CARERS protocol to help frontline staff manage disclosures from carers and third parties (From Vulnerability, GDPR, and disclosure: A practical guide for creditors and advisers)

Equally, affected others may benefit from help and support themselves to protect their money and wellbeing. A Citizens Advice survey found that 69% of affected others had to cover the costs or debts of the gambler – and in some cases felt coerced into this.

In the first year of the MAGPIE programme, we talked to many people with lived experience of gambling harm. One common theme was their desire for financial services firms and other professionals to develop a better understanding of gambling disorder and gambling harm. In the words of one participant: “Banks and financial institutions need to be educated about the illness [of disordered gambling]”. This is one of the areas we will focus on in our second MAGPIE project – a practical guide to help financial services firms better understand and support people affected by gambling.

Information and help for people affected by someone else’s gambling:

Information and help for people with gambling disorder:

By David Collings, Sharon Collard and Jamie Evans

Back in July we published a review of bank card gambling blockers – a feature that allows a debit or credit card customer to block their account or card from being used for gambling transactions. Working with GambleAware, we evaluated the potential for these blockers to help those who want to control their gambling.

Our review brought together bank data on customer use of blockers; discussions with treatment providers, firms and regulatory bodies; and, crucially, insights from over 100 interviews and surveys with people who have lived experience of gambling. It showed that blocker technology works and can help people control their gambling spend, but card blockers need to be more widely available than is currently the case. And, where offered, their design should incorporate elements of ‘positive friction’ in the form of ‘cooling-off’ periods.

At the time our report was written, eight firms advertised and offered blockers to their customers either on credit cards, debit cards or both. These include five of the nine largest banks and building societies in the UK – Barclays, HSBC, Lloyds, Royal Bank of Scotland Group and Santander – together with three other banks – Cashplus, Monzo and Starling.

We estimated that gambling blocks on debit cards are available for roughly 60% of personal current accounts (around 49 million accounts) and at least 40% of credit card customers (roughly 26 million cards). But if Santander and the Royal Bank of Scotland Group were to offer gambling blockers to all their debit card customers, we estimate that blockers would be available for around 90% of current accounts (equivalent to 70 million accounts – 22 million more than at present).

Increasing availability of these blocks isn’t enough on its own. Our findings show that blockers need to include ‘positive friction’ in the form of ‘cooling-off’ periods – to encourage time and reflection before someone can gamble again – in order to be effective.

As the table above shows, five of the eight firms offering blockers included a cooling-off period – a period after a customer disables the block before they can gamble again – while the remaining three blockers could immediately be toggled on and off, meaning they functioned more like a light switch than a lock.

But this is a fast-changing landscape. In September Barclays announced it is introducing a 72 hour cooling-off period to its gambling blocker, responding to customer feedback about the positive impact of such a delay, making it the first bank to introduce a cooling-off period off this length. This customer feedback echoes findings from our research, where nearly 60% of respondents with lived experience of gambling felt that a cooling-off period should be longer than 48 hours.

In fact, the message from those affected by gambling was clear: the more positive friction that can be built into a bank blocker, the better. Our research also explored other examples of positive friction that could be beneficial, including making gambling blocks the default on new bank cards, or automatic alerts for third parties such as a friend or family member related to gambling spend.

Our interviews with banks highlighted three main motivations for developing and implementing gambling blocks: ‘soft’ pressure from regulators; evidence of customer harm from gambling; and market ‘peer pressure’ as other banks launched gambling blocks for their card customers.

We therefore reiterate our call on the Financial Conduct Authority as part of its forthcoming guidance on the fair treatment of vulnerable customers to recommend that gambling blocks are standard on all credit and debit cards and require customers to wait at least 48 hours between turning off the blocker and being able use that card to gamble.

Finally, introducing gambling blockers shouldn’t be seen as ‘job done’ for banks and building societies – there is much more work to do and the purpose of our three-year MAGPIE research programme is to help progress that agenda. Similarly, other organisations beyond banks still need to be taking robust action to reduce gambling harms.

This blog was originally posted on the Money and Mental Health Policy Institute blog. Read the original post here.

By Sharon Collard, Jamie Evans and Chris Fitch

Our review of bank card gambling blockers published today shows they can be an effective way to help people control their spending on gambling. To make sure more people can benefit from this technology, all banks and credit card firms should offer blockers as a standard feature on their cards, with a time-released lock of at least 48 hours and the option to limit cash withdrawals.

A lot has happened since September 2019 when we officially launched the ‘Money and Gambling: Practice, Insight, Evidence (MAGPIE)’ programme funded by GambleAware. With the COVID-19 crisis ongoing, there are concerns that regular online gamblers have gambled more during lockdown; while both the House of Commons and the House of Lords have called for urgent reform of gambling regulation so that children, young people and adults are properly protected from gambling harm.

Our review of bank card gambling blockers shows they can help people control their gambling spend but they need to be much more widely available. While eight UK financial firms offer gambling blocks as standard to customers with a credit or debit card (see Table 1 below), as many as 28 million personal current accounts and 35 million credit cards may not have this option. We believe that blockers should be a standard feature available to all card holders across a firm’s full card range.

There is also work to be done to make sure people know about bank card gambling blocks. Nearly half of our survey participants (43%) – many of whom were receiving treatment and support for their gambling – were not aware that bank gambling blocks exist.

The design of bank card blockers is critical to their effectiveness. Some can be toggled on and off by customers at will – making them a light switch rather than a lock. Our review shows that a time-released lock of at least 48 hours should be a standard feature on all blockers – something the House of Lords also supports. To complement gambling blockers on cards, we want to see customers given the option to limit their ATM withdrawals. A ‘third line of defence’ could be the option to block cash transfers from a credit card to an account where the money could be used to gamble.

Despite the Gambling Commission’s recent ban on licensed gambling companies accepting credit card payments, we believe that every credit card should still offer gambling blocks. This is because online gambling sites outside of Britain are not licensed by the Gambling Commission and continue to allow customers in England, Wales and Scotland to gamble via credit card payments. Credit card providers could go one step further by automatically restricting gambling on all credit cards, rather than relying on customers to turn on a block. Even then, there remains a risk that unscrupulous gambling operators engage in ‘transaction laundering’ which renders a gambling block ineffective.

Gambling blocks can help but they are not enough. People with experience of gambling harms want to see financial firms take wider action if they are serious about helping tackle this public health issue. Beyond banks, they want the gambling industry, regulators and the Government to do much more to protect consumers in a world of boundless and frictionless gambling where, in the words of one participant, it is possible to go from “zero to devastation in a very short period”.

Read the report:

A Blueprint for Bank Card Gambling Blockers – Report | A Blueprint for Bank Card Gambling Blockers – Executive Summary

By Jamie Evans and Sharon Collard

Yesterday’s move by the Gambling Commission to ban gambling using credit cards is a welcome public health intervention and one that now shifts the focus onto other ways for people to control their gambling spend. ‘Spending controls’, offered by a growing number of banks, provide one such solution, giving customers the option to block gambling transactions from their accounts. But how can banks maximise the effectiveness of such controls? In this blog, we provide an update from our strategic partnership with GambleAware, which aims to answer this and other questions about the potential role of financial services firms in reducing gambling-related harm.

In September 2019, we officially launched ‘Money and Gambling: Practice, Insight, Evidence (MAGPIE)’ – a three-year programme between the University of Bristol’s Personal Finance Research Centre (PFRC) and GambleAware, a charity who fund research, prevention and treatment into the harms of gambling. The programme is designed to explore and improve the way that financial firms tackle gambling-related harm.

Since then, we have been busy working on the first of several projects within the programme. This considers how ‘spending controls’ – otherwise known as ‘gambling blocks’ – that are available on a growing number of debit and credit cards can be as effective as possible in reducing gambling-related harm. To do this, we have conducted expert interviews with banks and other key stakeholders; consulted people affected by gambling through Advisory Boards and interviews; and reviewed academic and other literature on this topic.

We are also working with banks that have launched spending controls to understand patterns in customer data and are running an online survey of people affected by gambling to find out more about their views and experiences of spending controls. Collectively, we hope the new data collected from these different sources will help improve the industry’s understanding of what does and doesn’t work when it comes to spending controls.

Customers of several UK financial services firms now have access to gambling blocks on their accounts (as shown in the below diagram) – and we know of at least one other firm that offers a similar service on request if you telephone them. Blocks on credit card transactions should, in theory, be unnecessary once the wider ban on gambling with credit cards is introduced in April 2020.

The diagram shows that gambling blocks differ in terms of their ‘cooling off’ period (i.e. the length of time after choosing to turn off a gambling block that someone would have to wait until they can gamble again on their account). Some currently offer no cooling-off period, which means that a customer could use the card to gamble as soon as they turn off the block. CashPlus and HSBC both have a 24 hour cooling off period; while Lloyds Banking Group (including Lloyds Bank, Halifax, Bank of Scotland and MBNA) and Monzo require customers to wait 48 hours before they can gamble again.

This cooling-off period is generally recognised, by banks and treatment providers, as a crucial component of an effective gambling block – especially for customers engaged in more high-risk gambling behaviours. As such, we are very likely to see more firms incorporating this kind of ‘friction’ into their spending controls in the near future.

While obviously important, our work recognises that an effective gambling block is about more than just its cooling-off period. Friction can come in many forms and there are some really interesting ideas on the horizon about the shape that these could take.

There are also a range of other fascinating, albeit challenging, questions that we need to answer. For example, we need to understand more about the customer’s engagement with staff if and when they try to turn off the block, or what happens if they try to gamble when the block is turned on. How are gambling blocks being communicated to customers, and how do financial services firms reach the right people? Who even are the ‘right people’?! It might be the case that a whole spectrum of products and services should be made available to customers engaging in a wide range of gambling behaviours, including those who might not be engaged in risky gambling behaviours right now but may do so in future.

And there are questions that may stretch beyond the usual remit of the financial services sector. How, for example, might unscrupulous gambling operators try to circumvent such spending controls, and – crucially – what can we do about this?

There exists a rich body of academic literature about gambling and ways to reduce gambling-related harm. To bring this literature to a wider audience – including financial services firms – we have published a Roadmap which sets out the rationale for our programme and summarises some of the existing evidence that is relevant to spending controls. It highlights, for example, the importance of viewing spending controls as one tool in a wider harm minimisation toolkit, as well as the importance of considering the other people affected by gambling (such as partners, families, friends) and the help and support they might require from financial services firms.

You can read this roadmap document here and sign-up for updates about the programme here.

The University of Bristol’s Personal Finance Research Centre (PFRC) is today pleased to announce the launch of Money and Gambling: Practice, Insight, Evidence (MAGPIE), a new three-year strategic programme, in partnership with Gamble Aware, which looks at the role that financial services organisations can play in reducing gambling-related harm.

Gambling problems can destroy lives, often leaving those affected to live with severe financial and social consequences. Indeed, around seven in ten people seeking help for gambling problems report that they are in debt, with a third of these owing £10,000 or more. Between 2007 and 2014 there were an average of 500 bankruptcies per year known to be linked to gambling – the true figure, however, may be much higher because people may not disclose that their bankruptcy is related to gambling.[1]

While many people do enjoy gambling safely, the number of people who are ‘problem gamblers’ or who suffer negative consequences as a result of their gambling is far from insignificant. It is estimated that in 2016 nearly a million adults in Britain experienced sizeable negative consequences as a result of their gambling, with around 360,000 adults classified as ‘problem gamblers’ (Gambling Commission, 2019).

Money and gambling are clearly intricately linked, with ‘gambling more than you can afford’ one of the key indicators of a gambling problem. As such, it makes sense that organisations that help us look after our money – the world of ‘financial services’ – might also be able to take actions to help those at-risk of gambling-related harm.

Such firms are regulated by the Financial Conduct Authority (FCA), which in recent years has upped its focus on the way that companies treat customers in vulnerable situations – including those living with gambling problems. As a result, firms are paying increased attention to the way that they identify and support such customers.

Indeed, in 2016, PFRC conducted research with over 1,500 frontline debt collection staff working in a wide range of financial services firms, including high-street banks, lenders and debt collection agencies. This research focused on staff members’ experiences of working with customers in vulnerable situations, including those with mental health problems, suicidal thoughts and addictions, and highlighted some of the challenges that they face – whether in identifying ‘vulnerability’, starting a conversation about it, or providing customers with adequate support or sign-posting to other sources of support.

Following that research, we held a number of ‘problem-solving workshops’ with firms, charities and those with lived experience of different vulnerable situations to develop new tools and guidance for debt collection staff when working with such customers. Many of the solutions developed have now been adopted (or, in some cases, even adapted) by firms – highlighting the fact that there is considerable appetite among those working in financial services to do what they can to help such customers.

Last year saw the introduction of spending controls or ‘gambling blocks’ by several UK banks – most notably Barclays, Monzo and Starling. Once turned on by customers, these essentially prevent spending on a bank card at gambling outlets (both online or in-person).

We know that people in recovery from problem gambling already use informal workarounds to prevent themselves from spending money on gambling, such as forfeiting their card to a third party or scratching off the card security number. The new solutions from banks, however, allow customers to do this more formally – and, possibly, more successfully.

But at present there is limited evidence about the effectiveness of such spending controls, nor about the characteristics of those who use them. We also don’t know much about the unintended consequences of these spending blockers (for example, whether it leads to customers withdrawing more money as cash and gambling with that).

As such, the first six months of our programme will focus on answering these questions and building the evidence-base around what works for recovering gamblers. We will use this evidence to produce practical guidance for financial services firms around the design of spending blockers.

In order to build the evidence-base, we’ll be working closely throughout the project with financial services firms – but, more importantly, our research will place those with lived experience of problem gambling at the centre of the project, as well as those with expertise in the treatment of recovering gamblers.

So, if you’re interested in being part of the research or if you simply want to be kept updated, you can join our money and gambling network by filling out this short form.

Notes:

GambleAware is an independent charity that champions a public health approach to preventing gambling harms. The charity is a commissioner of integrated prevention, education and treatment services on a national scale, with over £40 million of grant funding under active management. In partnership with gambling treatment providers, GambleAware has spent several years methodically building structures for commissioning a coherent system of brief intervention and treatment services, with clearly defined care pathways and established referral routes to and from the NHS – a National Gambling Treatment Service. Follow GambleAware on Twitter: @GambleAware

GambleAware also runs the website BeGambleAware.org which helps 4.2 million visitors a year and signposts to a wide range of support services. Follow BeGambleAware on Twitter: @BeGambleAware

[1] See RGSB (2015) Understanding gambling-related harm and debt. Available at: https://www.rgsb.org.uk/PDF/Understanding-gambling-related-harm-and-debt-July-2015.pdf